Current issue

Online first

Archive

About the Journal

Aims and scope

Editorial Board

International Editorial Board

List of Reviewers

Abstracting and indexing

Ethical standards and procedures

REMV in Social Media

Contact

Instructions for Authors

Instructions for Authors

Manuscript formatting template

Title page

Highlights

Payments

‘Ghostwriting’ and ‘Guestauthorship’

Guidelines for Referees

Global information uncertainty and real estate stock valuation in emerging markets: An integrated behavioral - Theoretical and machine learning framework

1

Faculty of Banking, Ho Chi Minh University of Banking (HUB), Vietnam

Submission date: 2025-06-09

Final revision date: 2025-09-25

Acceptance date: 2025-09-30

Publication date: 2026-03-17

REMV; 2026;34(1):63-83

HIGHLIGHTS

- models real estate valuation using behavioral and machine learning methods

- introduces esg, geopolitical, and policy uncertainty indices into pricing model

- applies shap and lime to interpret nonlinear and size-based pricing effects

- finds inverse u-shape between firm size and global uncertainty index

- builds a transparent ai framework for asset pricing in emerging markets

KEYWORDS

information uncertaintyESGuncertaintybehavioral asset pricingreal estate stocksemerging marketsmachine learning

TOPICS

- C45 - Neural Networks and Related Topics

- C53 - Forecasting and Prediction Methods • Simulation Methods

- D84 - Expectations • Speculations

- G12 - Asset Pricing • Trading Volume • Bond Interest Rates

- G14 - Information and Market Efficiency • Event Studies • Insider Trading

- R33 - Nonagricultural and Nonresidential Real Estate Markets

ABSTRACT

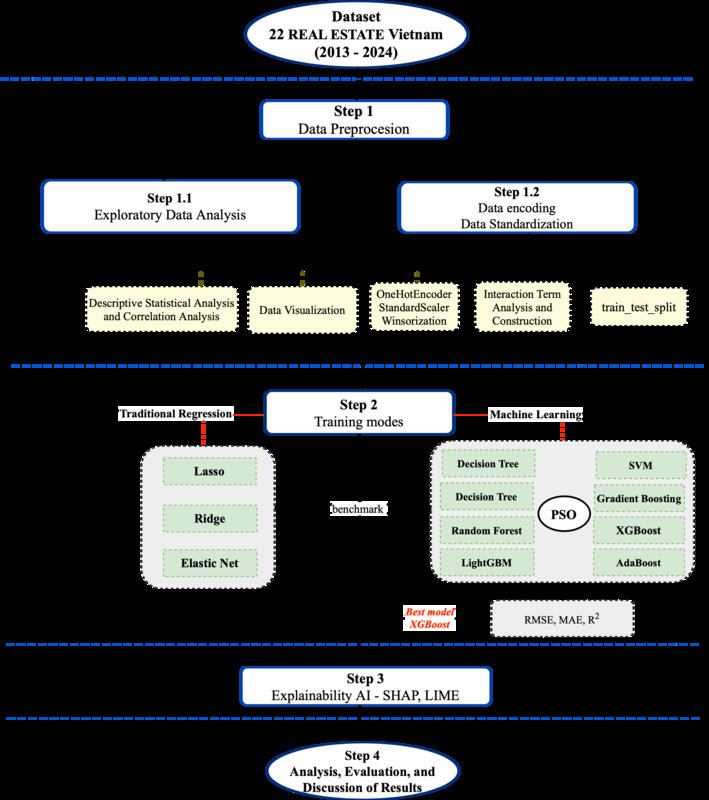

This study develops an integrated behavioral-theoretical and explainable machine learning framework to investigate how global information uncertainty affects real estate stock valuation in emerging markets. Grounded in Knightian uncertainty and behavioral finance theory, the analysis employs a panel dataset of 28 listed Vietnamese real estate firms from 2013 to 2024, incorporating firm fundamentals, macroeconomic controls, and four key uncertainty indices: ESG Uncertainty (ESGUI), Geopolitical Risk (GPR), World Uncertainty (WUI), and Media Sentiment (WSI). Nonlinear predictive models, particularly XGBoost optimized via Particle Swarm Optimization (PSO), are interpreted using SHAP and LIME to uncover both global and local effects. Results indicate that firm size and book value are the most influential valuation drivers, while global uncertainty indices demonstrate conditional effects. Notably, the interaction between WUI and firm size reveals an inverse U-shaped pattern, supporting the “asymmetric ambiguity response” hypothesis: under heightened uncertainty, investors gravitate towards large firms. The proposed framework offers theoretical consistency, predictive accuracy, and interpretability, contributing to the literature on asset pricing under uncertainty. Findings provide practical insights for ESG communication, risk mitigation, and regulatory design in opaque and sentiment-sensitive emerging markets.

Share

RELATED ARTICLE

| eISSN: | 2300-5289 |

We process personal data collected when visiting the website. The function of obtaining information about users and their behavior is carried out by voluntarily entered information in forms and saving cookies in end devices. Data, including cookies, are used to provide services, improve the user experience and to analyze the traffic in accordance with the Privacy policy. Data are also collected and processed by Google Analytics tool (more).

You can change cookies settings in your browser. Restricted use of cookies in the browser configuration may affect some functionalities of the website.

You can change cookies settings in your browser. Restricted use of cookies in the browser configuration may affect some functionalities of the website.