Current issue

Online first

Archive

About the Journal

Aims and scope

Editorial Board

International Editorial Board

List of Reviewers

Abstracting and indexing

Ethical standards and procedures

REMV in Social Media

Contact

Instructions for Authors

Instructions for Authors

Manuscript formatting template

Title page

Highlights

Payments

‘Ghostwriting’ and ‘Guestauthorship’

Guidelines for Referees

Identification of Regularities in Relation Between Prices on Primary and Secondary Housing Market in Selected Cities iIn Poland

1

Faculty of Economics and Management, University of Szczecin, Poland

Submission date: 2022-02-04

Final revision date: 2022-03-24

Acceptance date: 2022-04-19

Publication date: 2022-09-22

Corresponding author

REMV; 2022;30(3):45-60

HIGHLIGHTS

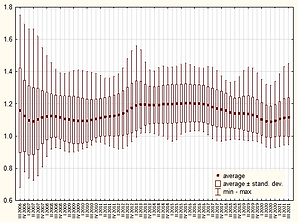

- w większości poddanych badaniu miast ceny mieszkań na rynkach pierwotnych są wyższe od cen na rynkach wtórnych. Jednak nie są rzadkie sytuacje w których okresowo (niekiedy sporadycznie) bywa odwrotnie. Tylko dla Warszawy średnia wartość WRCW z całego badanego okresu była niższa od 1, a dla 10 miast wskaźnik ten nigdy nie zszedł do poziomu poniżej 1. Wskaźniki na ogół cechowały się dużą zmiennością, ich maksymalne wartości przekraczały 1,7, a za wartości typowe należy uznać przedział od 1,0 do 1,2

- relacje między cenami mieszkań na rynkach pierwotnych i wtórnych nie są trwałe i ulegają relatywnie dużym, nieregularnym wahaniom w czasie. Tylko dla 4 miast rozstęp wartości WRCW w badanym okresie był mniejszy niż 0,2. Dla 4 też był większy niż 0,4

- w poszczególnych miastach przebiegi WRCW były różne – zarówno co do wartości jak i pod względem okresów wzrostowych i spadkowych wartości wskaźników. Można wyróżnić grupy miast względnie podobnych pod względem wartości WRCW, lecz nie są to podobieństwa silne. W poszczególnych grupach miast podobnych pod względem WRCW znajdują się miasta zróżnicowane pod względem wielkości i położenia geograficznego (np. w jednej grupie jest Warszawa i Olsztyn, w innej Kraków i Opole itp.)

- wartości średnie WRCW obliczone ze wszystkich miast nie wykazują analogii do ogólnej sytuacji na rynku wtórnym i pierwotnym, w szczególności ich przebieg w czasie nie wpasowuje się w cykle spadków i wzrostów cen mieszkań,

- statystycznie istotne, ale generalnie nie silne związki pomiędzy wartościami WRCW a charakterystykami wielkości istniejącego i nowopowstającego zasobu mieszkaniowego odnotowano tylko dla 9 miast. Jednak tylko dla 3 z nich kierunek związku był ujemny (zgodnie z oczekiwaniami), a dla 6 dodatni. W pozostałych 8 miastach nie odnotowano statystycznie istotnych związków

KEYWORDS

TOPICS

ABSTRACT

The purpose of this study is to identify regularities in the price relations between primary and secondary housing markets. The primary market and the secondary market are two related but quite differentiated sub-segments of the residential market. They particularly differ in the qualitative features of their traded objects and, consequently, also in the prices recorded in their trading. Nevertheless, they remain under the influence of the same main factors of a macroeconomic nature. This gives rise to the research hypothesis that prices of flats quoted in the sub-segments of the residential market remain in specific relationships with one another.

In an attempt to verify this hypothesis, the paper presents the results of an analytical work on the search for regularities in the relationship between prices on primary and secondary housing markets in selected Polish cities. The regularities concern the dynamics and structure of price relation indices constructed for the research. They also include classification analyses. The findings of the research have revealed, inter alia, that in the majority of the cities under study, prices of flats in the primary markets are higher than prices in the secondary markets. However, situations in which the reverse happens periodically (sometimes occasionally) are not rare. The examined relations are not permanent and are subject to relatively large, irregular fluctuations over time. It is possible to distinguish groups of cities which are relatively similar in this respect, but these similarities are not strong.

Share

RELATED ARTICLE

| eISSN: | 2300-5289 |

We process personal data collected when visiting the website. The function of obtaining information about users and their behavior is carried out by voluntarily entered information in forms and saving cookies in end devices. Data, including cookies, are used to provide services, improve the user experience and to analyze the traffic in accordance with the Privacy policy. Data are also collected and processed by Google Analytics tool (more).

You can change cookies settings in your browser. Restricted use of cookies in the browser configuration may affect some functionalities of the website.

You can change cookies settings in your browser. Restricted use of cookies in the browser configuration may affect some functionalities of the website.