Current issue

Online first

Archive

About the Journal

Aims and scope

Editorial Board

International Editorial Board

List of Reviewers

Abstracting and indexing

Ethical standards and procedures

REMV in Social Media

Contact

Instructions for Authors

Instructions for Authors

Manuscript formatting template

Title page

Highlights

Payments

‘Ghostwriting’ and ‘Guestauthorship’

Guidelines for Referees

Editor's Choice

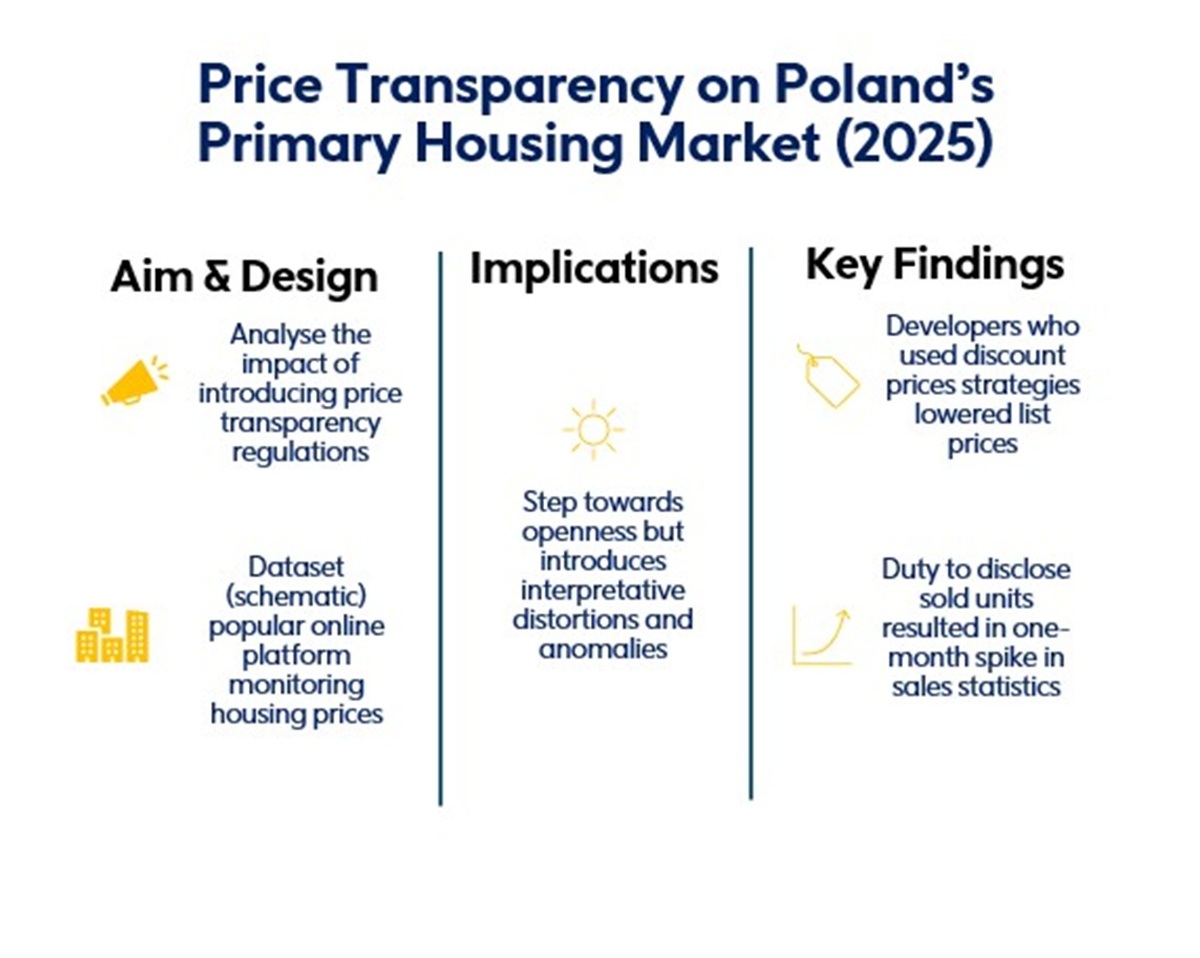

Illusion of transparency: Short-term effects of price disclosure regulations on the Polish primary residential market

1

Wrocław University of Economics and Business, Poland

These authors had equal contribution to this work

Submission date: 2025-10-06

Final revision date: 2025-12-19

Acceptance date: 2026-03-07

HIGHLIGHTS

- the lack of price transparency causes problems in the property market

- non-standard data limit comparability

- transparency law triggered widespread repricing

- early effects skewed toward list-price cuts, not fundamental shocks

- 2025 reform reduced key info asymmetry but only partly improved transparency

KEYWORDS

TOPICS

ABSTRACT

The study investigates short-term market adjustments following the introduction of price transparency requirements in Poland’s primary housing sector. Using a dataset of 57,041 dwellings across 23 cities and focusing on six major agglomerations, it analyzes how developers modified list prices and reporting practices during the 2025 rollout period.

Results indicate that developers visibly repriced a large share of their inventories around key implementation dates, with the most pronounced activity in September 2025. In large urban markets, the adjustments were predominantly downward, reflecting strategic repositioning in anticipation of easier cross-project comparisons rather than shifts in demand fundamentals. These repricing waves temporarily reduced average list prices, creating misleading signals for less experienced market participants. The analysis also highlights the persistence of data inconsistencies and definitional ambiguities that limit comparability across projects. Despite greater public access to pricing information, uneven data quality continues to constrain accurate monitoring and interpretation of market dynamics. Consumers benefited from faster access to headline prices, yet analysts and smaller developers remained exposed to information gaps. Overall, the findings suggest that while transparency can promote more informed market behaviour, its effectiveness depends on robust data standards, auditability mechanisms, and the integration of verified transaction-level evidence.

| eISSN: | 2300-5289 |

We process personal data collected when visiting the website. The function of obtaining information about users and their behavior is carried out by voluntarily entered information in forms and saving cookies in end devices. Data, including cookies, are used to provide services, improve the user experience and to analyze the traffic in accordance with the Privacy policy. Data are also collected and processed by Google Analytics tool (more).

You can change cookies settings in your browser. Restricted use of cookies in the browser configuration may affect some functionalities of the website.

You can change cookies settings in your browser. Restricted use of cookies in the browser configuration may affect some functionalities of the website.