Current issue

Online first

Archive

About the Journal

Aims and scope

Editorial Board

International Editorial Board

List of Reviewers

Abstracting and indexing

Ethical standards and procedures

REMV in Social Media

Contact

Instructions for Authors

Instructions for Authors

Manuscript formatting template

Title page

Highlights

Payments

‘Ghostwriting’ and ‘Guestauthorship’

Guidelines for Referees

Bridging predictive power and interpretability: A hybrid deep learning framework for real estate performance under systemic uncertainty

1

Ho Chi Minh University of Banking, Vietnam

These authors had equal contribution to this work

Submission date: 2026-01-08

Final revision date: 2026-02-26

Acceptance date: 2026-04-12

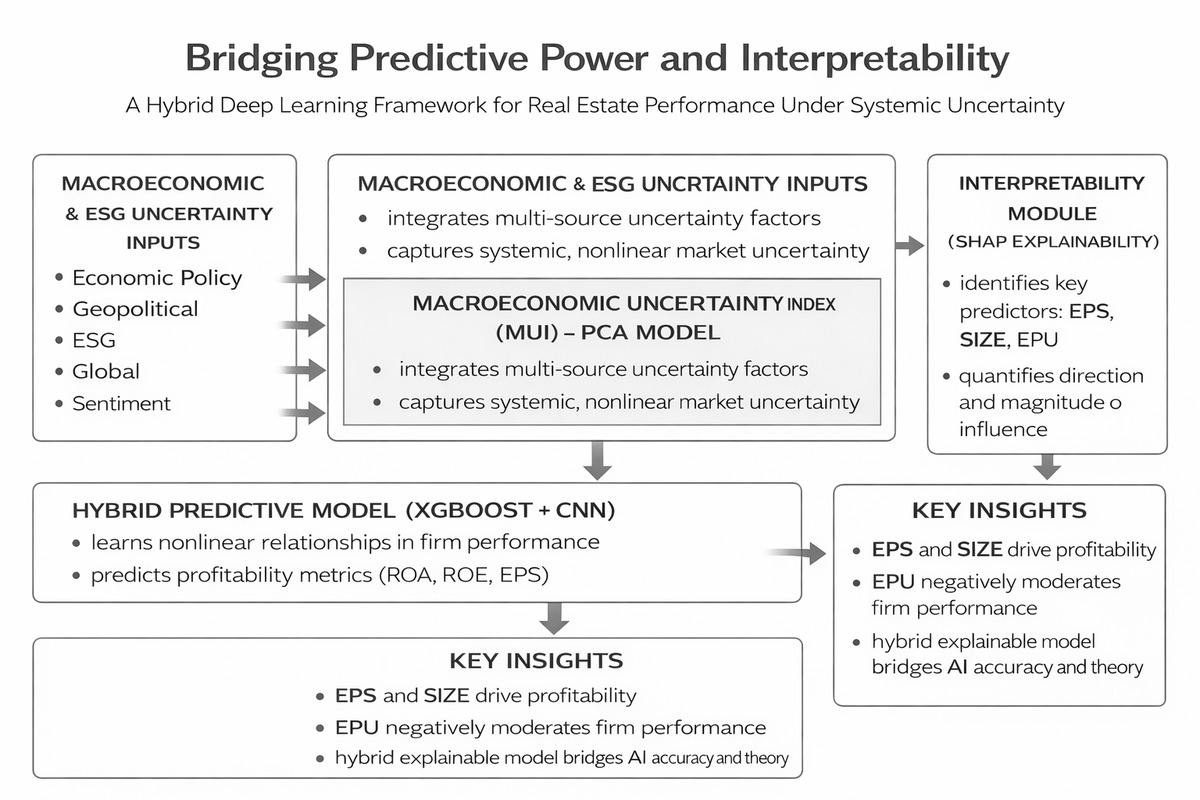

HIGHLIGHTS

- develops an interpretable hybrid xgboost–cnn model for real estate forecasting

- constructs a composite macroeconomic uncertainty index using PCA integration

- applies shap explainability to uncover firm and macro-level performance drivers

- finds eps and size dominate roe, while policy uncertainty exerts strongest effect

- bridges deep learning accuracy with economic theory for transparent forecasting

KEYWORDS

interpretable hybrid deep learningmacroeconomic uncertainty indexSHAP explainable AIfinancial performance forecastingemerging real estate markets

TOPICS

- C45 - Neural Networks and Related Topics

- C53 - Forecasting and Prediction Methods • Simulation Methods

- G17 - Financial Forecasting and Simulation

- G32 - Financing Policy • Financial Risk and Risk Management • Capital and Ownership Structure • Value of Firms • Goodwill

- R33 - Nonagricultural and Nonresidential Real Estate Markets

ABSTRACT

This study develops an interpretable hybrid deep learning framework to forecast and explain the financial performance of real estate firms in emerging markets facing macroeconomic uncertainty. Using panel data from 28 listed Vietnamese firms during 2013–2025, a Macroeconomic Uncertainty Index (MUI) is constructed through principal component analysis to integrate five global risk indicators: economic policy, geopolitical, ESG-related, global uncertainty, and world sentiment indices. The proposed XGBoost–CNN model, augmented with SHAP explainability, achieves superior predictive accuracy, reducing RMSE by 54 percent and MAE by 22 percent compared with conventional deep learning models. SHAP analysis, applied to both the composite and individual uncertainty components, enhances interpretability and isolates the marginal influence of each risk factor. Results indicate that earnings per share and firm size jointly explain most of the variation in return on equity and assets, while economic policy uncertainty exerts the strongest macroeconomic impact. The MUI demonstrates a nonlinear moderating role, showing that, under heightened systemic uncertainty, traditional firm–performance relationships may reverse. The framework offers a transparent, data-driven tool for financial forecasting and macroprudential stress testing in emerging real estate markets.

| eISSN: | 2300-5289 |

We process personal data collected when visiting the website. The function of obtaining information about users and their behavior is carried out by voluntarily entered information in forms and saving cookies in end devices. Data, including cookies, are used to provide services, improve the user experience and to analyze the traffic in accordance with the Privacy policy. Data are also collected and processed by Google Analytics tool (more).

You can change cookies settings in your browser. Restricted use of cookies in the browser configuration may affect some functionalities of the website.

You can change cookies settings in your browser. Restricted use of cookies in the browser configuration may affect some functionalities of the website.